A Guide to Help You Purchase Reverse Mortgage for Your Retirement Plan

A Guide to Help You Purchase Reverse Mortgage for Your Retirement Plan

Blog Article

Step-By-Step: How to Purchase a Reverse Home Loan With Self-confidence

Browsing the intricacies of buying a reverse home mortgage can be challenging, yet an organized method can empower you to make enlightened choices. It begins with examining your qualification and recognizing the subtleties of various lending options offered in the market (purchase reverse mortgage). As we check out each action, it ends up being apparent that confidence in this monetary choice pivots on thorough prep work and educated options.

Comprehending Reverse Mortgages

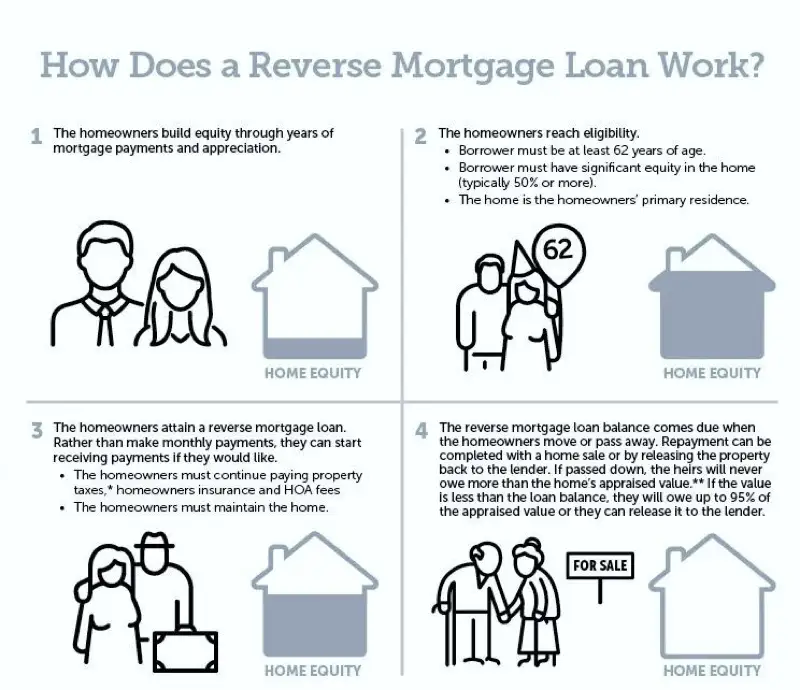

The key system of a reverse mortgage involves loaning versus the home's worth, with the loan amount raising gradually as rate of interest accumulates. Unlike traditional mortgages, customers are not called for to make month-to-month settlements; rather, the financing is paid back when the home owner sells the residential property, moves out, or dies.

There are 2 main kinds of reverse mortgages: Home Equity Conversion Home Loans (HECM), which are federally guaranteed, and proprietary reverse home mortgages used by personal lending institutions. HECMs normally offer higher protection as a result of their governing oversight.

While reverse home loans can use economic alleviation, they likewise feature costs, including origination fees and insurance policy premiums. Consequently, it is critical for potential consumers to completely recognize the terms and effects before waging this financial choice.

Analyzing Your Qualification

Eligibility for a reverse mortgage is primarily identified by several key factors that prospective customers must take into consideration. Applicants need to be at the very least 62 years of age, as this age requirement is set to make certain that consumers are approaching or in retirement. Furthermore, the home has to act as the consumer's primary house, which indicates it can not be a holiday or rental property.

Another vital aspect is the equity setting in the home. Lenders commonly call for that the borrower has an enough amount of equity, which can influence the quantity available for the reverse home loan. Typically, the more equity you have, the bigger the loan amount you might get approved for.

In addition, possible borrowers have to demonstrate their capability to fulfill economic commitments, consisting of residential or commercial property tax obligations, house owners insurance coverage, and maintenance expenses - purchase reverse mortgage. This evaluation often includes a financial evaluation carried out by the lending institution, which evaluates income, credit report, and existing financial obligations

Last but not least, the building itself have to fulfill particular criteria, including being single-family homes, FHA-approved condos, or certain manufactured homes. Comprehending these elements is important for determining qualification and planning for the reverse home mortgage process.

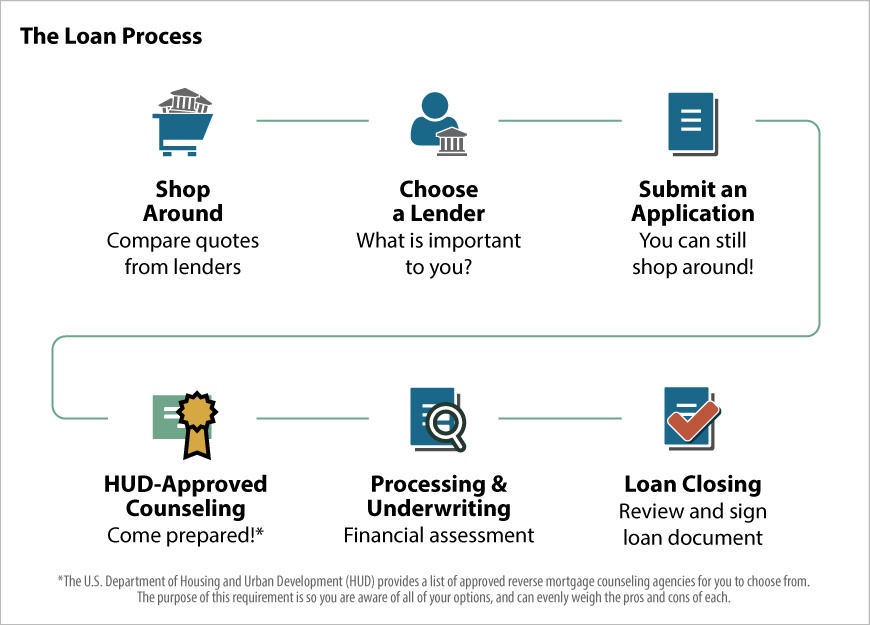

Investigating Lenders

After identifying your qualification for a reverse home loan, the next action entails researching lenders that supply these monetary products. It is vital to determine respectable loan providers with experience in reverse home loans, as this will guarantee you get dependable guidance throughout the process.

Begin by reviewing lender credentials and accreditations. Seek loan providers who are participants of the National Opposite Mortgage Lenders Association (NRMLA) and are authorized by the Federal Real Estate Management (FHA) These associations can indicate a commitment to honest methods and compliance with industry criteria.

Reading customer reviews and testimonies can supply understanding into the loan provider's credibility and client service high quality. Websites like the Bbb (BBB) can also offer scores and problem histories that may aid notify your choice.

In addition, seek advice from with economic experts or real estate therapists that specialize in reverse mortgages. Their know-how can assist you navigate the alternatives readily available and suggest trustworthy lenders based upon your unique economic circumstance.

Comparing Lending Choices

Contrasting financing choices is a vital action in securing a reverse mortgage that aligns with your economic goals. When evaluating different reverse home mortgage items, it is important to take into consideration the specific features, expenses, and terms related to each alternative. Start by reviewing the kind of reverse home mortgage that best matches your demands, such as Home Equity Conversion Mortgages (HECM) or exclusive loans, which might have various qualification standards and advantages.

Following, pay attention get redirected here to the rates of interest and fees connected with each car loan. Fixed-rate financings offer security, while adjustable-rate options may offer reduced preliminary rates but can vary with time. In addition, take into consideration the ahead of time costs, consisting of home mortgage insurance coverage costs, origination charges, and closing expenses, as these can significantly influence the general expenditure of the funding.

In addition, evaluate the settlement terms and just how they align with your long-term financial technique. When the financing have to be paid back is crucial, recognizing the effects of just how and. By completely comparing these factors, you can make an educated choice, ensuring your choice sustains your financial health and wellbeing and offers the safety you seek in your retirement years.

Completing the Purchase

When you have actually carefully evaluated your choices and picked one of the most ideal reverse mortgage product, the following action is to finalize the purchase. This procedure entails several vital actions, ensuring that all needed paperwork is properly completed and submitted.

First, you will certainly need to collect all needed documents, consisting of evidence of income, residential property tax declarations, and property owners insurance coverage paperwork. Your lender will give a checklist Web Site of specific records needed to assist in the approval process. It's essential to provide full and precise info to avoid hold-ups.

Following, you will certainly go through a comprehensive underwriting process. During this phase, the loan provider will certainly examine your financial scenario and the worth of your home. This may include a home appraisal to identify the building's market price.

When underwriting is complete, you will get a Closing Disclosure, which describes the last terms of the funding, including charges and rate of interest. Testimonial this paper meticulously to make sure that it aligns Continued with your expectations.

Verdict

To conclude, browsing the process of buying a reverse home mortgage calls for an extensive understanding of eligibility requirements, attentive research study on lenders, and mindful comparison of finance options. By systematically complying with these actions, individuals can make enlightened decisions, guaranteeing that the picked mortgage straightens with monetary objectives and demands. Eventually, a well-informed method cultivates confidence in securing a reverse mortgage, supplying economic stability and support for the future.

Look for loan providers that are participants of the National Reverse Home Loan Lenders Organization (NRMLA) and are approved by the Federal Real Estate Administration (FHA)Contrasting loan alternatives is a vital step in safeguarding a reverse mortgage that lines up with your monetary objectives (purchase reverse mortgage). Begin by evaluating the type of reverse home mortgage that finest suits your requirements, such as Home Equity Conversion Home Loans (HECM) or proprietary financings, which might have different eligibility standards and advantages

In conclusion, browsing the procedure of acquiring a reverse mortgage requires an extensive understanding of qualification requirements, persistent study on loan providers, and careful comparison of finance options. Eventually, a knowledgeable approach fosters self-confidence in securing a reverse home mortgage, providing monetary stability and support for the future.

Report this page